Since June 2020, Australia approved 1,056,669 new dwellings — 665,380 houses, 219,133 units, and 172,156 townhouses — worth approximately $461 billion. But where are they being built, and what type? Victoria is the undisputed national champion with 326,854 total dwelling approvals — 208,352 houses, 57,382 units, and 61,120 townhouses — equal to 31% of the national total. NSW ranks second (287,131 total dwellings), with the nation's largest unit pipeline (83,282 units — more than Victoria). Queensland ranks third (213,812 total dwellings). Below we rank all states and territories by total dwelling approvals, and break down the mix of houses, units, and townhouses defining each region's character and investment risk.

🥇 Victoria: 326,854 Total Dwellings — Australia's #1 State

Top unit hotspots: Docklands (5,410) · Port Melbourne (3,059) · Footscray (2,281)

Houses: 208,352 · Units: 57,382 · Townhouses: 61,120

Total dwellings: 326,854 · Total value: $146.1B

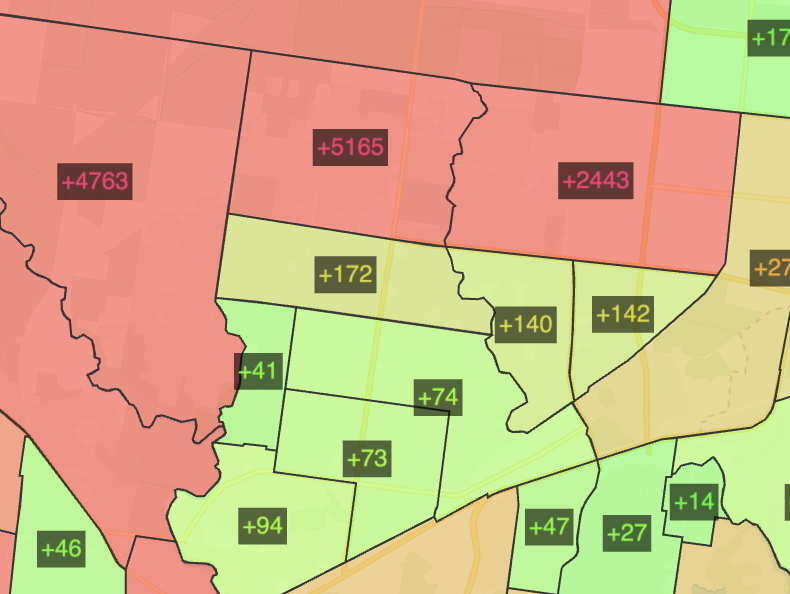

Victoria's western fringe is the single largest residential construction zone in Australia. Rockbank–Mount Cottrell in Melton led the entire country with 9,739 house approvals, while neighbouring Fraser Rise–Plumpton added 8,764 — together representing 9% of all Victorian house approvals. VIC also leads on townhouse approvals (61,120), though NSW edges it slightly on unit approvals (83,282 vs 57,382). Stockland's "Atherstone" (~6,500 lots), Satterley's "Eliston" (~3,000 lots), and multiple Cedar Woods and Peet estates define this corridor. Tarneit–North in Wyndham followed with 5,165 approvals, where Stockland's "Riverwalk" (~4,000 lots), AVID's "Harpley", and RCM Property's premium "Wyndham Harbour" marina estate operate. Melton and Wyndham City Councils consistently rank among Australia's fastest-growing LGAs; Infrastructure Victoria has repeatedly flagged that roads, schools, and hospitals have lagged behind residential delivery.

Melbourne's northern suburbs are anchored by MAB Corporation and Gibson Property Corporation's "Merrifield" at Mickleham — Australia's largest mixed-use development combining ~6,000 residential lots with the 870-hectare Merrifield Business Park. Mickleham–Yuroke generated 7,675 house approvals. Nearby Wollert and Whittlesea–Wallan contributed 5,127 and 5,056 approvals respectively, with Stockland's "Edgebrook" (~3,000 lots) and Peet's "Wallara Waters" (~3,000 lots at Wallan, 60 km from the CBD) active in this corridor. The Melbourne Airport Rail Link, under construction from approximately 2024, is expected to transform connectivity for Tullamarine and Broadmeadows.

The Casey South growth corridor — Clyde North (6,977) and Cranbourne South (5,261) — is catering strongly to first-home buyers and the area's large Vietnamese-Australian community. Stockland's "Meridian" (~5,500 lots) and Mirvac's "Circa" (~3,000 lots) are the marquee estates, with the Pakenham Rail Line serving the corridor.

Melbourne's inner west is also transforming. Docklands generated 5,410 unit approvals, led by Lendlease's "Collins Wharf" (premium waterfront towers, 30+ storeys) and Mirvac's "Yarra's Edge" and "NewQuay" final stages. Meanwhile Footscray accumulated 2,281 unit approvals, driven by the Victorian Government's Activity Centre Program and Caydon Property Group's towers near the new Footscray Hospital (opened 2023).

🏠 New South Wales: 287,131 Total Dwellings

Top unit hotspots: Schofields East (4,305) · Macquarie Park–Marsfield (3,815) · Castle Hill Central (3,597)

Houses: 143,954 · Units: 83,282 · Townhouses: 59,895

Total dwellings: 287,131 · Total value: $130.9B

Sydney's north-west has become the nation's most concentrated greenfield corridor. Box Hill–Nelson alone recorded 6,253 house approvals (4.3% of all NSW house approvals) as Rouse Hill, Box Hill, Marsden Park, Riverstone, and Schofields generated a combined 18,000+ house approvals. Notably, NSW leads the nation on unit approvals (83,282), exceeding Victoria's unit pipeline (57,382). Key estates include Stockland's "The Gables" (Box Hill North, ~3,000 lots), Stockland's "Altrove" at Schofields (~4,500 lots), and Sekisui House's "Elara" at Marsden Park (~3,000 lots). These suburbs are served by the Sydney Metro Northwest (opened 2019) and sit within the NSW Department of Planning's North West Priority Growth Area.

The Schofields East transit corridor has also generated 4,305 unit approvals, driven by the NSW Government's 2024 Transport Oriented Development SEPP which rezoned land within 400–800m of the station for high-density towers. This represents the first major wave of mandatory apartment zoning around rail stations outside the inner city.

Sydney's south-west is the state's other major greenfield frontier. Austral–Greendale (5,145 approvals), Leppington–Catherine Field (3,394), and Oran Park (1,830) form a continuous corridor southwest of Liverpool. The centrepiece is Oran Park Town, developed by Greenfields Development Company, one of Australia's largest master-planned communities at ~11,000 lots across 2,000 hectares. Cedar Woods, Satterley, and AVID Property Group hold the neighbouring land parcels at Gledswood Hills and Leppington. The South West Rail Link (Leppington station) opened in 2015 to support the corridor, though infrastructure capacity remains a recurring concern among residents.

Inner Sydney continues to densify. Macquarie Park–Marsfield tallied 3,815 unit approvals anchored by Mirvac's "Lachlan's Line" precinct (1,100+ apartments, 6–24 storeys) and TOGA/UEM Sunrise towers along Herring Road. Castle Hill Central recorded 3,597 unit approvals following the Metro Northwest's arrival, with Deicorp's "Crestwood Rise" (~900 apartments) among the standout projects. Zetland and Wentworth Point–Sydney Olympic Park added another 2,877–3,052 units each.

🏠 Queensland: 213,812 Total Dwellings

Top unit hotspots: Mermaid Beach–Broadbeach (3,308) · Surfers Paradise North (3,013) · Brisbane City (2,403)

Houses: 137,707 · Units: 47,606 · Townhouses: 28,499

Total dwellings: 213,812 · Total value: $98.1B

Queensland's dominant house-approval area is Ripley in Greater Ipswich (5,626 house approvals, 4.1% of the state's dwelling pipeline). The Ripley Valley Priority Development Area is planned for 120,000 residents at full build-out. AVID Property Group's "Harmony" estate (~4,000 lots) and Sekisui House's "Ecco Ripley" (~2,700 homes, 6-star Green Star community design) anchor the precinct, alongside Consolidated Properties' Ripley Town Centre hub.

Caloundra West–Baringa on the Sunshine Coast generated 3,765 house approvals as part of Stockland's "Aura" — currently Australia's largest masterplanned community under construction, with 20,000+ homes and 50,000+ residents planned at full build-out. Baringa was the first suburb to open (~2017) and by 2026 is well into its mid-stages, with Nirimba and Bokarina Beach precincts following. The estate includes its own primary and secondary schools (opened 2019–21), a business park, and 100+ km of walking and cycling trails.

Between Brisbane and the Gold Coast, the Logan growth corridor is one of Queensland's most active. Chambers Flat–Logan Reserve (3,290 house + 1,069 townhouse approvals) and Greenbank–North Maclean (3,140 approvals) are dominated by Peet Limited's "Covella" estate (~3,200 lots) and Sekisui House's "Flagstone" PDA (~25,000+ total capacity). Boronia Heights–Park Ridge contributed 2,997 house approvals and 794 townhouse approvals, primarily from Villaworld and Frasers Property medium-density product.

The Gold Coast's apartment pipeline is led by Mermaid Beach–Broadbeach (3,308 unit approvals) and Surfers Paradise North (3,013), where 20–50 storey towers from developers including Consolidated Properties and DVB Developments delivered premium coastal product. Inner Brisbane — Brisbane City (2,403), South Brisbane (2,017), Newstead–Bowen Hills (1,722), and West End (1,640) — continues its transformation with Mirvac's "Newstead Riverpark" precinct, Aria Property Group's towers, and Pradella's "West Village" urban renewal (1,000+ apartments across multiple stages).

🏠 Western Australia: 112,720 Total Dwellings

Top unit hotspots: Subiaco–Shenton Park (1,773) · Applecross–Ardross (794)

Houses: 95,493 · Units: 11,083 · Townhouses: 6,144

Total dwellings: 112,720 · Total value: $44.6B

Western Australia's busiest growth zone runs along Perth's northern coast, where Alkimos–Eglinton in the City of Wanneroo led the state with 5,544 house approvals. The area is home to Peet Limited's "Allara" (~3,500 lots, Alkimos), Stockland's "Amberton" (~4,000 lots, Eglinton with its private Amberton Beach Club), and LWP Property Group's "Shorehaven" (~2,000 lots with a central lake). The Yanchep Rail Extension opened in December 2022, reducing commute times to Perth CBD substantially. Brabham–Henley Brook in the City of Swan added 3,270 approvals, supported by LWP's "Brabham" estate (~4,500 lots), and the new Ellenbrook rail line opened in 2024.

The Rockingham corridor is Perth's other major growth axis. Baldivis North and South generated 3,075 and 2,105 house approvals respectively with Peet's "Settlers Hills" and Cedar Woods' "Crossways" estates attracting families. Mandurah North contributed 3,020 approvals — Peet's "Lakelands" (~5,000 lots, golf course) and the Mandurah Rail Line make this Perth's coastal southern satellite.

Perth's inner ring is also densifying. Subiaco–Shenton Park led unit approvals with 1,773, driven by the WA Government's "Subi East" urban renewal program — transforming the former Subiaco Oval and QEII Medical Centre sites into 2,500–3,000 premium dwellings, linked to the Subiaco Station Quarter METRONET upgrade.

🏠 South Australia: 72,730 Total Dwellings

Top unit hotspots: Adelaide City (1,070) · Toorak Gardens (530)

Houses: 56,243 · Units: 5,159 · Townhouses: 11,328

Total dwellings: 72,730 · Total value: $25.8B

South Australia's residential growth is heavily concentrated in the Playford Council area north of Adelaide. Munno Para West–Angle Vale led with 5,134 house approvals — a remarkable 9.1% of the entire state's dwelling pipeline concentrated in one area. Villawood Properties' "Buckland Park" (~9,000+ dwellings planned, $3 billion investment) spans the Virginia–Angle Vale boundary and is among Australia's most ambitious regional residential projects outside the major capitals. Virginia–Waterloo Corner added 2,296 further approvals, supported by the Northern Connector motorway and proximity to the Edinburgh RAAF Base.

Mount Barker in the Adelaide Hills accumulated 3,049 house approvals since June 2020, driven by Hickinbotham Group's estates ("Verdant Hills", "The Heights Mount Barker") — SA's largest private residential developer. The Mount Barker Development Plan Amendment extended growth boundaries for a region with 14,000 planned new dwellings over 30 years. Though positioned 35 km from the Adelaide CBD and offering tree-change lifestyle appeal, major SA Water infrastructure upgrades have been required.

Adelaide's middle ring is producing a townhouse boom, with Plympton (584), Mitchell Park (583), Woodville–Cheltenham (582), and Warradale (462) each recording significant approvals as the 30-Year Plan for Greater Adelaide unlocks medium-density infill in established suburbs. Adelaide CBD itself generated 1,070 unit approvals as the city's apartment market responds to student accommodation demand from the University of Adelaide and UniSA campuses.

🏠 Australian Capital Territory: 24,436 Total Dwellings

Top unit hotspots: Phillip/Woden (2,706) · Gungahlin (1,505) · Belconnen (1,469) · Denman Prospect (1,266)

Houses: 5,948 · Units: 14,133 · Townhouses: 4,355

Total dwellings: 24,436 · Total value: $8.3B

Note: The ACT is the only state/territory where units outnumber houses.

The ACT is unique: it is the only Australian state or territory where unit approvals (14,133) outnumber house approvals (5,948). This reflects a dramatic shift toward apartment-centric development, driven by inner-city densification and limited land for greenfield suburbs. In Gungahlin, Taylor led house approvals with 1,242 (20.9% of all ACT house approvals) — developed through the ACT Suburban Land Agency's land release program with the territory's unique Land Rent Scheme. In the Molonglo Valley, Whitlam (883) and Denman Prospect (521) are delivering ~7,000 and ~5,500 dwellings across an entirely new district flanked by the Molonglo River Reserve and Stromlo Forest Park (2023 Commonwealth Games venue). Denman Prospect alone generated 761 townhouse and 1,266 unit approvals.

Phillip–Woden Valley recorded 2,706 unit approvals as Geocon's "Grand Central Towers" and Doma Group redevelop this 1960s town centre ahead of the planned Light Rail Stage 2 extension. Inner Canberra (Braddon, Turner, Dickson, Lyneham) has emerged as a boutique apartment hub with 2,500+ unit approvals since June 2020, reinforcing the ACT's position as the nation's apartment-first development market.

🏠 Tasmania: 16,383 Total Dwellings

Houses: 15,433 · Units: 393 · Townhouses: 557

Total dwellings: 16,383 · Total value: $6.0B

Tasmania's dwelling growth is almost entirely concentrated in Greater Hobart. Rokeby in Clarence City led with 827 house approvals, followed by the Sorell–Richmond corridor (709 house approvals) as Hobart's acute housing shortage (median prices exceeded $600,000 by 2022) pushed demand into the eastern and southeastern fringes. Kingston–Huntingfield in Hobart's south contributed 368 house and 137 townhouse approvals, reflecting medium-density development responding to the Tasmanian Government's "Housing Tasmania" strategy. Hobart inner city recorded 225 unit approvals — modest in absolute terms, but significant for a city of its size. With only 393 unit approvals and 557 townhouse approvals statewide, Tasmania's pipeline is heavily weighted toward houses (94% of total dwellings).

🏠 Northern Territory: 2,603 Total Dwellings

Houses: 2,250 · Units: 95 · Townhouses: 258

Total dwellings: 2,603 · Total value: $1.1B

The Northern Territory's residential pipeline is the smallest of any state or territory. Palmerston South stands out with 738 house approvals — 32.8% of the entire NT house total. The suburb cluster of Zuccoli, Mitchell, and Bellamack is NT's largest masterplanned community, driven by Frasers Property/ABN Group's "Zuccoli" (~2,500 lots) and strong Defence Housing Australia demand from Robertson Barracks (Army base). In Alice Springs, Mount Johns and Ross contributed 75 combined townhouse approvals — small in absolute numbers but significant locally given the town's documented acute housing shortage. At just 2,603 total dwellings since June 2020, the NT's entire dwelling pipeline is smaller than many individual suburbs in the larger states.

The Risks of Investing in Oversupplied Residential Areas

High approval numbers don't guarantee returns. Investors should be aware of six material risks in concentrated development corridors:

1. Settlement and completion risk. Multiple volume builders collapsed in 2022–23 (Porter Davis, Probuild, Privium, ABD Group), leaving buyers with partly-built homes and progress payments at risk. In Ripley, Ipswich, and Perth fringe suburbs where one or two developers dominate, a builder failure can cascade through the entire precinct.

2. Infrastructure lag. Schools, hospitals, and public transport routinely trail population growth by 2–5 years in outer corridors (Melbourne West, Ipswich, Perth North). This depresses lifestyle quality and short-term rental demand as families defer moves until schools open.

3. Rental vacancy and yield compression. In concentrated precincts (Docklands, Surfers Paradise, Wentworth Point), high unit delivery in short windows can suppress rents. Investor yields in these areas have fallen from 4–5% (2020) to 2–3% (2026) as thousands of new apartments compete for tenants.

4. Resale liquidity risk. Greenfield estates with thousands of identical lots hitting the resale market simultaneously — especially in single-income-market towns (Palmerston/Defence, Ripley/Ipswich) — can depress resale prices. New apartment markets are particularly vulnerable to this "launch overhang" effect.

5. Capital growth lag. Outer fringe greenfield properties typically underperform inner-ring and established suburb capital growth over 10-year horizons, even if initial purchase prices are lower. Inner Melbourne and Sydney have seen 8–12% annualised growth; outer precincts average 4–6%.

6. Concentration risk. Areas anchored to a single employer, infrastructure project, or developer carry outsized risk. Defence bases (Palmerston), airport expansion (Tullamarine), or a single developer's financial distress (Greenfields Development Company in Oran Park) can disrupt entire precincts.

The highest-risk areas are those combining multiple risk factors: remote location + single employer + single developer, or high-density + speculative international capital + limited rental demand.